导读:“It is a leech, a financial parasite in the banking system of China. It never created any value and only got the benefits by pulling up the financing cost of the whole society.”This is a quote from Ni...

“It is a leech, a financial parasite in the banking system of China. It never created any value and only got the benefits by pulling up the financing cost of the whole society.”

This is a quote from Niu Wenxin, an economic reviewer working for the CCTV. The “leech” and “financial parasite” he referred to was Yu E Bao, a financial product launched and promoted by Alibaba. It is a tool that allowed the users of online payment tool Alipay to use the balance of Alipay to buy the funds. The capital can be transferred in and out any time easily and the earnings are calculated on a daily basis.

The product Yu E Bao is quite young. It was born in June 2013 as a result of the cooperation between Ali- baba and Tianhong Fund. At that time, a voice immediately rose, saying that Yu E Bao was targeting none other than the commercial banks in China as the high interest rate it promised is going to be a strong magnet for the depositors.

However, the rich and never-facingcompetition commercial banks in China laughed at the notion and behaved extremely calmly. “They could not last long if they keep doing like that,” a senior executive of a state-owned commercial bank said confidently.

His disdain of Yu E Bao sounded reasonable. The 6% or higher interest rate the financial tool promised is to be a trouble if the collective cash-in happened. Commercial banks have the support from their peers. How can Yu E Bao, a tool of a company with tense fluidity, achieve the easy lending of money in the market? As speculated, the high interest rate is going to be the trump for attracting the deposits, but this, as the senior executive said, was abandoned by commercial banks several years ago.

Fermentation of the Rancor

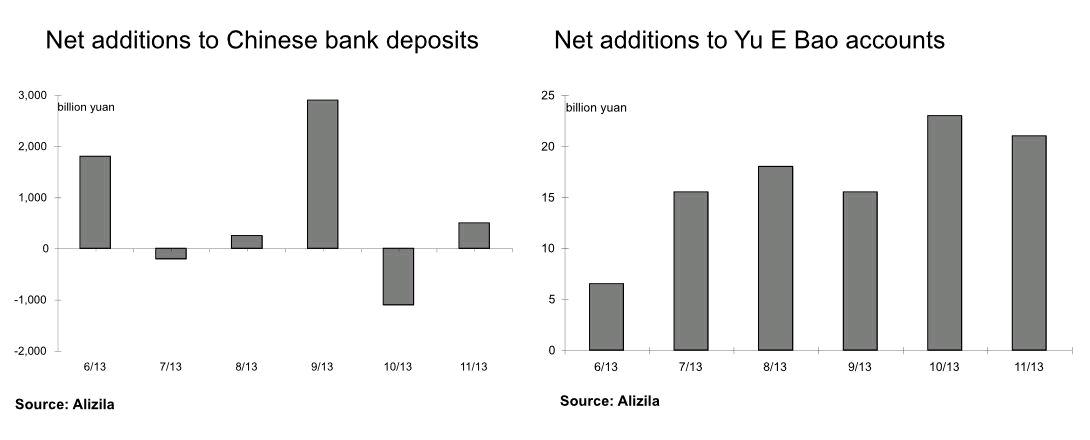

But six months later, the elites of commercial banks like this senior executive were slapped right in their faces. When the time got into the year of 2014, the banks suddenly – and shockingly – found that the deposits reserved in their saves reduced by 940.2 billion yuan. In the past, they could comfort themselves with the thought that depositors needed to take out their money for the approaching Spring Festival.

But the truth is not that comforting. As shown from the data, Yu E Bao is really a contributor to the loss of the deposits of banks. In the six monthsdevelopment, more than 49 million accounts were registered with the raised funds of 250 billion yuan. In only half a year, Yu E Bao finished what China AMC has done in 15 years.

Many bank workers admitted that the rise of online financial products have moved the deposits from banks. Qiu Guanhua, a researcher from Guotai Securities, said that the online finance has distracted 5% of the capital from banks and lower the income of traditional banking business by 1%. From last November, some large banks had to borrow money from other banks with the interest rate of 6%-8%.

Whats worse is that there are more than Yu E Bao. Tecent, a well-established IT company launched its own financial tool attached to its popular instant communication tool WeChat. The rancor between banks and Yu E Bao has been evolved to the battle between Internet and banks.

That could be a pain for the Chinese commercial banks, which never met serious challenges in the past decades. But this time, the Internet has indeed beamed a threat against them. They are panicking and anxious, which could explain Niu Wenxins consideration of Yu E Bao as a “leech”.

As an economist, Niu Wenxin did not say that out of his personal hatred for Yu E Bao. He admitted that the rise of Yu E Bao brought a great impact to the banks. However, he followed by saying when the Chinese citizens are happy with the more profits from their deposits in Yu E Bao, they never expect that the companies they are working for are facing the increasing cost of fundraising, which might devour their opportunities of salary increase or even destabilize their jobs.

“I am not exaggerating or overstating the truth. I am not either calling for you to abandon Yu E Bao. I just want to tell you an important economic truth. Yu E Bao does not only impact the banks, but also is going to push up the financing cost of Chinas society, which is to be a threat for the Chinese economic safety,” said Niu Wenxin.“Thats because Yu E Bao and its frontend monetary fund put 2% earnings into their own pockets while sharing the 4%-6% earnings with their users. In that way, the Chinese real economy, which is the borrower of loans from Yu E Bao, are eventually those to pay the bills.”

He also admitted that the banks have unreasonable huge profits, but he insisted that the huge banking profits, if to be eliminated, should be given back to Chinese enterprises involved in the real economy, instead of allocating them to the “financial parasite” like Yu E Bao.

“Japan is also known for the high deposit ratio, just like China. But I have never heard of similar things like Yu E Bao in Japan,” he added. “In my opinion, any economy, or any financial regulators with a bit intelligence, should ban Yu E Bao without any hesitation, because it severely impacted the interest rate market and severed the fluidity of banks, leading to higher financing cost of enterprises of real industry. This could be a great threat for the financial and economic security of China.”

We cannot deny that Mr. Niu has said something right, but what he did not realize that the banks he defended are the real “vampires”. For long, their low interest rate for depositors and high interest rate for enterprises, especially private enterprises, are one of the real reasons for the stagnant private economy and real economy in China. In addition, the banks are known to be extremely rigorous when it comes to lending money to private enterprises, especially the small ones, which almost cut the access of these companies to loans. Yu E Bao could save them even though they might pay higher interest rate.

In addition, the ordinary users could have earned more from Yu E Bao, allowing them to spend more in the future. The increase in the consumption is definitely good news for the Chinese economy which relies on the investment too much at this moment.

And, like an Internet user said, “the banks cannot do nothing helpful just by yelling at Yu E Bao. They need to take actions to take the deposits back from Yu E Bao.”

The Counterstrike of Banks

The banks have already done it. On January 24, the branch of Agricultural Bank of China (ABC) in Jiangsu announced through its Microblog that it is going to increase the fixed-term deposit interest rate to the upper limit, which will remain valid till March 20. Outside of Jiangsu, many branches of ABC in Beijing and Shanghai are also told to implement the same measure as well.

According to an insider from ABC, the fixed-term deposit interest rate is going to be floated up by 10%, as long as the deposited amount exceeds 10 thousand yuan. This change covers all kinds of fixed-term deposits whose terms range from three months to five years. “In this year, the interest rate for one-year deposit could be increased from 3.25% to 3.3%. The changed interest rate allowed the depositors to earn additional 50 yuan per month after saving 100 thousand yuan,” said the insider.

Since June 2012 when Chinas central bank allowed commercial banks to adjust the interest rate to be 1.1 times as the base interest rate fixed by the central bank. It is the origination of the maximally 10% interest rate increase. At first, most commercials made full use of the scope. But with the goal of evading furious competition, the top five banks –ABC, Industrial and Commercial Bank of China (ICBC), Bank of China (BOC), China Construction Bank (CCB) and Bank of Communications (BOCOM) –kept their deposit interest rate to be 8% higher than the benchmark rate under the guidance of the central bank.

But this time, even the top five banks sensed the crisis. As ABC broke the ice, BOCOM is reported to work on the similar plans as well – some branches in Shanghai have already released the news that the interest rate for 3- and 5-year deposits could be increased by 10%. CCB also increased its interest rate, but it abandoned the pattern of universal interest rate for every part of China; instead, different places have different requirements for the terms, categories and minimum amounts of deposits when it comes to the increase of interest rate. The official website of CCB showed that this is the result of the pricing system combining the standardization and differentiation, which give different branches more authority and is good for the reasonable distribution.

The counterstrikes of banks are not limited to the increase of interest rate. The banks, which are not fools, immediately sensed that Yu E Bao and other Internet financial tools could rise so quickly because of their easy trade process and high yield. China Merchant Bank took the lead – and soon followed by ICBC and ABC – in limiting the amount that users could move money from their bank accounts to Yu E Bao.

Then, the banks are still restless. They launched their own “Yu E Bao”one by one. BOCOM launched a product named “Kuai Yi Tong” in 2013. Recently, ICBCs Zhejiang branch worked with UBS Credit to introduce a new monetary fund.

“Promoting the products similar to Yu E Bao is a spontaneous reform for banks. If the deposit continued to flow out massively, it is better for us to change ourselves than watching the money leave,” said an insider from ICBC.

以上就是小编为大家介绍的The Panicking Banks的全部内容,如果大家还对相关的内容感兴趣,请持续关注上海建站网!

标签:

内容声明:网站所展示的内容均由第三方用户投稿提供,内容的真实性、准确性和合法性均由发布用户负责。上海建站网对此不承担任何相关连带责任。上海建站网遵循相关法律法规严格审核相关关内容,如您发现页面有任何违法或侵权信息,欢迎向网站举报并提供有效线索,我们将认真核查、及时处理。感谢您的参与和支持!